Intelligent Investment

Fewer Renter Households Can Afford Homeownership

September 15, 2025 2 Minute Read

Approximately 1.8 million U.S. renter households can no longer afford the median-priced home in their market due to less affordability of homeownership over the past five and a half years. The primary drivers of this unaffordability have been persistently high mortgage rates and sharply higher home prices.

With more renter households unable to afford homeownership, CBRE forecasts that multifamily occupancy rates will remain higher than historical averages for years to come. This in turn will put upward pressure on near-term rent growth as multifamily supply and demand rebalances.

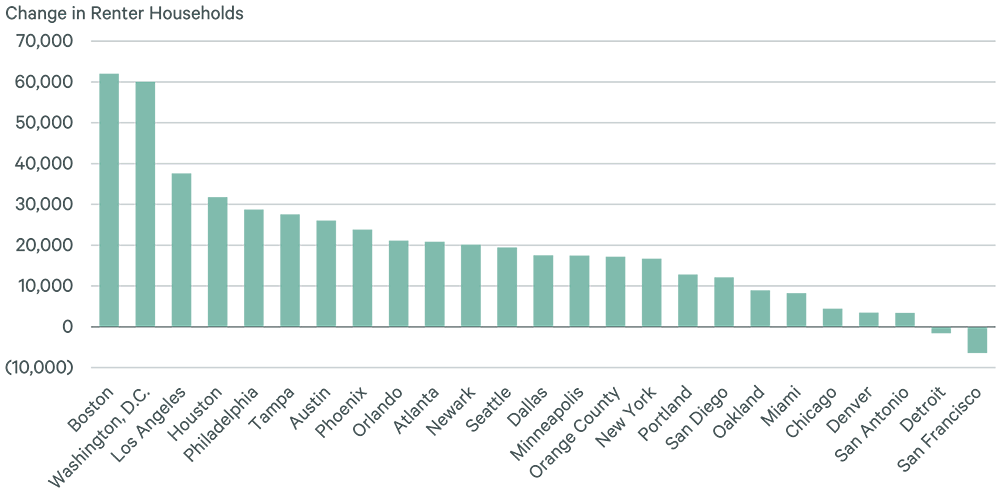

Figure 1: Renter Households That Can No Longer Afford a Median-Priced Home Due to Changes in Affordability

Source: CBRE Research, CBRE Econometric Advisors, U.S. Census Bureau, Realtor.com®, FHFA, NAR, Oxford Economics, Q2 2025.

Of the 69 markets tracked by CBRE, Boston and Washington, D.C. have the most renter households that can no longer afford a median-priced home. They are followed by other large markets such as Los Angeles and Philadelphia, as well as Sun Belt markets that saw significant in-migration during the COVID pandemic. Tampa, Austin, Phoenix, Orlando and Atlanta have seen some of the biggest increases in home prices due to the pandemic-era spike in demand. Though home prices in some of these markets are now either stable or have declined slightly, they will remain unaffordable to many renter households for years to come.

Figure 2: Percentage of Renter Households That Can Afford a Median-Priced Home in the 25 Largest Markets

To determine how many renter households can afford a median-priced home, CBRE estimated an all-in monthly cost (including mortgage, insurance, taxes and general maintenance) and compared that against renter incomes in each market. A threshold of 40% of gross monthly income was used to determine if the average payment for a median-priced home is affordable for a renter household. Based on this analysis, the proportion of U.S. renter households that can afford a median-priced home as of Q2 2025 dropped to just 12.7% from 17.0% in 2019. This equates to 1.8 million renter households that can no longer afford to purchase a median-priced home.

Markets with the biggest reductions in the percentage of renter households that can afford homeownership include Tampa (-10.1 percentage points) Washington, D.C. (-9.0) and Austin (-8.3). Some markets such as Denver, New York and Chicago saw very little reductions in the percentage of renter households that can afford home ownership due to a combination of higher incomes and relatively stable or slightly declining home prices. Other markets with an already low percentage of renter households that can afford homeownership had little room for further reductions. For example, Orange County renter households that can afford a median-priced home as of Q2 2025 fell to a record-low 1.0% from 6.3% in 2019.

Figure 3: Buying Premium for the 25 Largest Markets

Source: CBRE Research, CBRE Econometric Advisors, U.S. Census Bureau, Realtor.com®, FHFA, NAR, Oxford Economics, Q2 2025.

Much of the drop in affordability can also be gauged by the increased premium required to make a monthly mortgage payment vs. the average market rent. Orange County saw its premium nearly double to 303% as of Q2 2025 from 160% in 2019. Buying premiums in Austin and Los Angeles also increased significantly, while some markets (e.g., San Francisco and Chicago) changed very little from 2019.

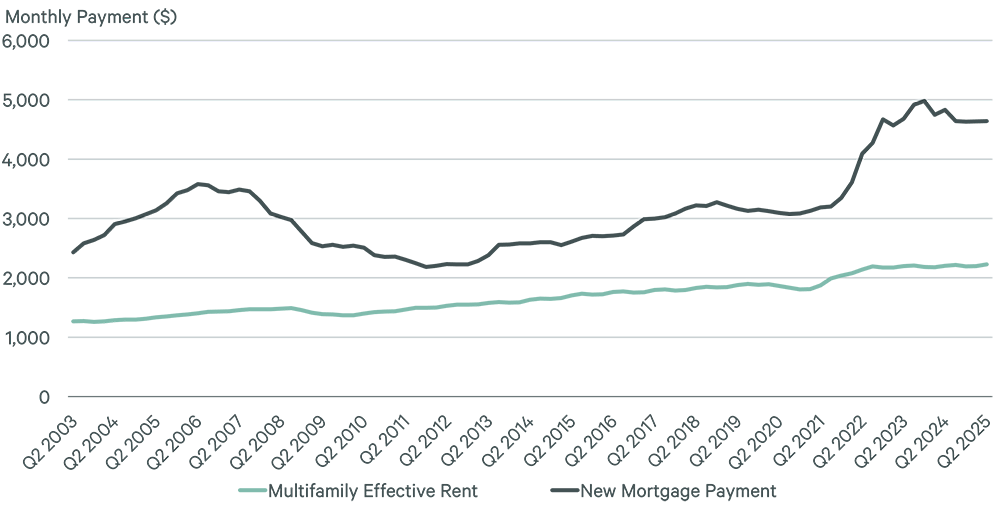

Figure 4: Average Monthly Multifamily Effective Rent vs. New Mortgage Payment

Source: CBRE Research, CBRE Econometric Advisors, U.S. Census Bureau, Realtor.com®, FHFA, NAR, Oxford Economics, Q2 2025.

While the buying premium remains significantly elevated over pre-pandemic levels in almost every U.S. market, it is slowly starting to drop. The national average buying premium is at 108% as of Q2 2025, down from 128% at year-end 2023 but still well above the 68% pre-pandemic average. The average monthly cost of buying a median-priced home was $4,643 as of Q2, more than double that of the average monthly rent of $2,228. CBRE estimates that a 20% down payment for the purchase of a home would cost the equivalent of four years of the average apartment rent. This grows to more than eight years in the most expensive markets like Orange County.

Eroding the spread between homeownership and renting requires a combination of lower home prices and interest rates, higher average incomes and strong rent growth. However, it will take years for the ownership-to-rent spread to return to more typical levels, leaving multifamily occupancy rates relatively high.

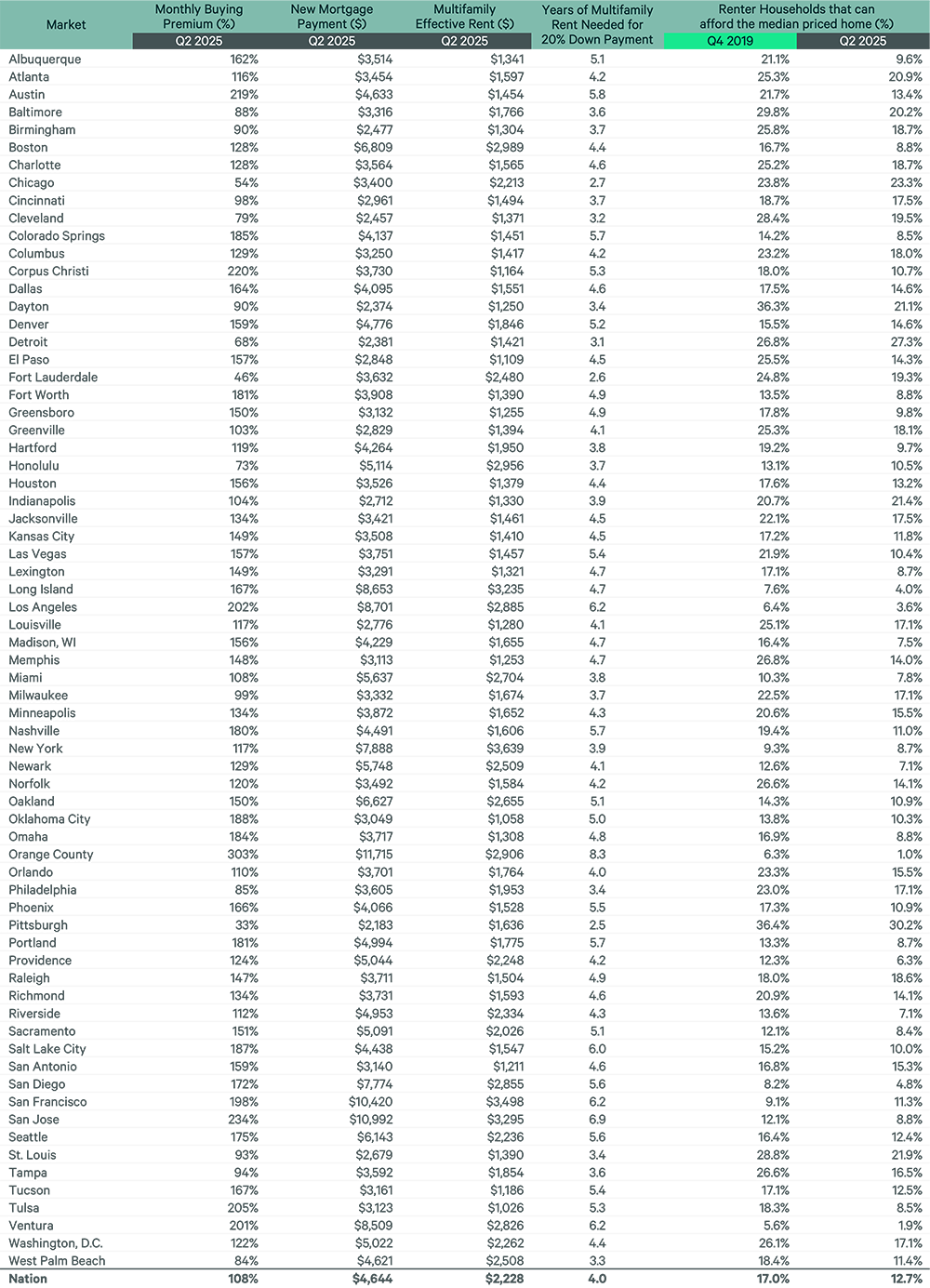

Figure 5: Cost of Buying vs. Renting Metrics by Market, Q2 2025

Related Insights

-

While economic uncertainty tempers growth, fundamentals remain healthy with pockets of outperformance across the industry.

Related Services

- Property Type

Multifamily

Unlock the potential of your residential real estate with expert investment, financing, valuation, due diligence, design, management and leasing strat...

- Invest, Finance & Value

Capital Markets

Gain proactive insights and strategies that unlock value, drive returns and enhance outcomes for your real estat...